#118 Marginal Gains - Part 4

“Something deep in the human heart breaks at the thought of a life of mediocrity.”

C.S. Lewis

Intellectual Diary of an Iconoclast | Annual Reviews

This review article, "The Political Economy of Decentralization in Developing Countries," by Jean-Paul Faguet and Jessica Seddon, published in the Annual Review of Political Science (2023), delves into the complex relationship between decentralization and development. The authors argue that while decentralization can enhance governance and service delivery, its success is contingent upon the political economy context in which it is implemented. They emphasize that the impact of decentralization is not homogenous and can vary significantly based on factors like the nature of political institutions, the distribution of power within a country, and the capacity of local governments.

Key Points and Explanations:

1. Decentralization is not a monolithic concept.

Explanation: The authors emphasize that decentralization encompasses a wide spectrum of reforms, each with its objectives and potential outcomes. They differentiate between various forms of decentralization, including political, administrative, and fiscal decentralization, highlighting the importance of understanding the specific type of decentralization being implemented.

Key Quote: "Decentralization is not a single, well-defined reform but rather a broad category encompassing a wide range of institutional changes."

Why it Matters: This point is crucial because it underscores the need to move beyond simplistic generalizations about decentralization. Treating all forms of decentralization as the same can lead to flawed policy prescriptions and unrealistic expectations.

2. The impact of decentralization is contingent upon the political economy context.

Explanation: This is the central argument of the review. The authors contend that the success of decentralization is not preordained but rather heavily influenced by a country's political and economic landscape. Factors such as the nature of the political system (democratic vs. authoritarian), state capacity, and power distribution between central and local elites play a critical role in shaping decentralization outcomes.

Key Quote: "The effects of decentralization are highly context-dependent and mediated by a range of political economy factors."

Why it Matters: This point highlights the danger of adopting a "one-size-fits-all" approach to decentralization. Policies designed without considering the specific political economy context are likely ineffective and may even exacerbate existing inequalities.

3. Decentralization can enhance service delivery, but it can also exacerbate inequalities.

Explanation: The review acknowledges the potential of decentralization to improve service delivery by bringing government closer to the people and allowing for more tailored policy responses. However, it also cautions that decentralization can increase regional disparities if not implemented carefully. This is particularly true in contexts marked by significant pre-existing inequalities and weak local capacity.

Key Quote: "Decentralization has the potential to improve the quality and responsiveness of public service delivery, but it can also exacerbate regional inequalities."

Why it Matters: This point emphasizes the need for a nuanced understanding of decentralization's potential benefits and risks. Policymakers need to carefully consider the distributional consequences of decentralization reforms and implement mechanisms to mitigate potential negative impacts on equity.

4. The design and implementation of decentralization reforms are critical.

Explanation: The authors stress that the success of decentralization hinges not only on the type of decentralization implemented but also on the specific design and implementation of reforms. This includes factors such as the clarity of responsibilities between different levels of government, the design of intergovernmental fiscal relations, and the mechanisms for ensuring accountability and citizen participation.

Key Quote: "The design and implementation of decentralization reforms are critical for determining their impact."

Why it Matters: This point underscores the importance of a strategic and context-specific approach to decentralization. Simply enacting decentralization laws is insufficient. Careful attention must be paid to implementation details to ensure that reforms achieve their objectives.

5. Political factors often outweigh technical considerations in shaping decentralization outcomes.

Explanation: The review highlights the significant influence of political factors on the trajectory and impact of decentralization. The distribution of power, political actors' incentives, and political competition are all crucial determinants of how decentralization unfolds in practice.

Key Quote: "Political factors often trump technical considerations in shaping the implementation and impact of decentralization."

Why it Matters: This point underscores the need for a politically informed approach to decentralization. Technical solutions alone are unlikely to be successful without addressing the underlying political dynamics that shape decentralization outcomes.

Conclusion:

The review concludes by emphasizing the need for a more nuanced and context-specific understanding of decentralization. While acknowledging its potential benefits, the authors caution against viewing it as a panacea for governance challenges. They argue that decentralization's success hinges on a complex interplay of factors, with political economy considerations playing a central role. The review provides a valuable framework for analyzing the complexities of decentralization and highlights the importance of adopting a context-sensitive approach to policy design and implementation.

💵 Warren Buffett’s $1 Test: A Simple Formula to Find Quality Companies (mailchi.mp)

This article, written by Vishal Khandelwal for his "Journal of Investing Wisdom" newsletter, introduces and analyzes Warren Buffett's "$1 Test" as a simple yet powerful tool for evaluating companies' value-creation ability.

Key Point 1: The Importance of Retained Earnings and Capital Allocation

The article begins by highlighting businesses' fundamental dilemma: distributing profits to shareholders through dividends or retaining them for future growth. When companies choose to retain earnings, it becomes crucial for investors to assess the effectiveness of management in utilizing these funds. This is where Buffett's $1 Test comes into play.

Key Quote: "Now, if the business is keeping that money, you as an owner better make sure the managers – the capital allocators – are using it well."

Explanation: Retained earnings represent the portion of profits a company reinvests back into its operations instead of paying out as dividends. These funds can be used for various purposes, such as expanding operations, acquiring new assets, research and development, or paying off debt. The effectiveness of capital allocation, i.e., how well management utilizes these retained earnings, directly impacts the company's future growth and profitability.

Why It Matters: For investors, understanding how effectively a company allocates capital is critical for assessing its long-term value creation potential. A company with skilled capital allocators can generate higher returns on invested capital, increasing shareholder value.

Key Point 2: The Essence of the $1 Test

The $1 Test, as described by Buffett, aims to determine whether a company is creating or destroying value for its shareholders. It compares the amount of earnings retained by the company over time with the increase in its market value.

Key Quote: "We test the wisdom of retaining earnings by assessing whether retention, over time, delivers shareholders at least $1 of market value for each $1 retained." (Warren Buffett, 1983 letter to shareholders)

Explanation: The test is straightforward:

Calculate the total earnings retained by the company over a specific period (e.g., 5 or 10 years).

Determine the change in the company's market capitalization over the same period.

Divide the change in market capitalization by the total retained earnings.

The company creates value for shareholders if the resulting multiple is greater than 1. If the multiple is less than 1, the company is destroying value.

Why It Matters: The $1 Test provides a simple yet powerful metric for evaluating a company's ability to translate retained earnings into tangible shareholder value. It cuts through the complexities of financial statements and focuses on the outcome: wealth creation for owners.

Key Point 3: Applying the $1 Test: Examples and Insights

The article provides practical examples of applying the $1 Test to three Indian companies: ITC, Asian Paints, and Voltas. It analyzes their performance over the past ten years and on a 5-year rolling basis.

Explanation: The analysis reveals that all three companies have generated significant value for shareholders over the past ten years, with multiples ranging from 8.7x to 14.1x. However, the picture becomes more nuanced when analyzed on a 5-year rolling basis. ITC's multiple has declined due to a surge in market capitalization in recent years, coupled with a generous dividend policy that reduced retained earnings. Asian Paints' multiple has also decreased due to subdued stock performance, while Voltas has benefited from strong stock performance in recent years.

Why It Matters: These examples demonstrate the importance of considering long-term and short-term trends when applying the $1 Test. Short-term fluctuations in stock prices can significantly impact the results, especially when analyzing a single period.

Key Point 4: Advantages and Limitations of the $1 Test

The article acknowledges both the advantages and limitations of the $1 Test.

Advantages:

Simplicity: The test is easy to understand and apply, even for investors with limited financial expertise.

Long-Term Focus: It encourages investors to evaluate a company's performance over time rather than focusing solely on short-term results.

Comparative Analysis: It facilitates quick comparisons between companies within an industry, helping identify those with superior value creation track records.

Limitations:

Stock Price Volatility: Short-term stock price movements can distort the results, particularly when analyzing a single period.

Industry Variations: Some industries require higher retained earnings for growth, potentially making them appear less efficient under the $1 Test.

Key Quote: "Of course, like all quick calculations that hide something behind their simplicity, even this metric suffers from disadvantages."

Why It Matters: Understanding the limitations of the $1 Test is crucial for avoiding misinterpretations and making informed investment decisions. It should be used as a starting point for further research and analysis, not as the sole basis for investment decisions.

Key Point 5: The $1 Test as a Starting Point for Deeper Analysis

The article emphasizes that the $1 Test is valuable for initial screening and identifying potentially high-quality companies. However, it should be complemented by other analytical methods for a comprehensive assessment.

Explanation: The $1 Test can help investors narrow their investment universe to companies with a track record of value creation. However, it does not provide insights into the underlying drivers of this value creation. To gain a deeper understanding, investors must explore factors such as return on invested capital, competitive advantages, management quality, and industry dynamics.

Why It Matters: The $1 Test should be viewed as a starting point for further research, not as a definitive indicator of investmentworthiness. By combining it with other analytical tools and a thorough understanding of the business, investors can make more informed and confident investment decisions.

Conclusion:

Warren Buffett's $1 Test offers a simple yet powerful framework for evaluating a company's ability to create shareholder value by effectively allocating retained earnings. While it has limitations, it is a valuable screening tool and a starting point for deeper analysis. By understanding the principles behind the test and applying it judiciously alongside other analytical methods, investors can enhance their ability to identify companies with strong long-term growth potential.

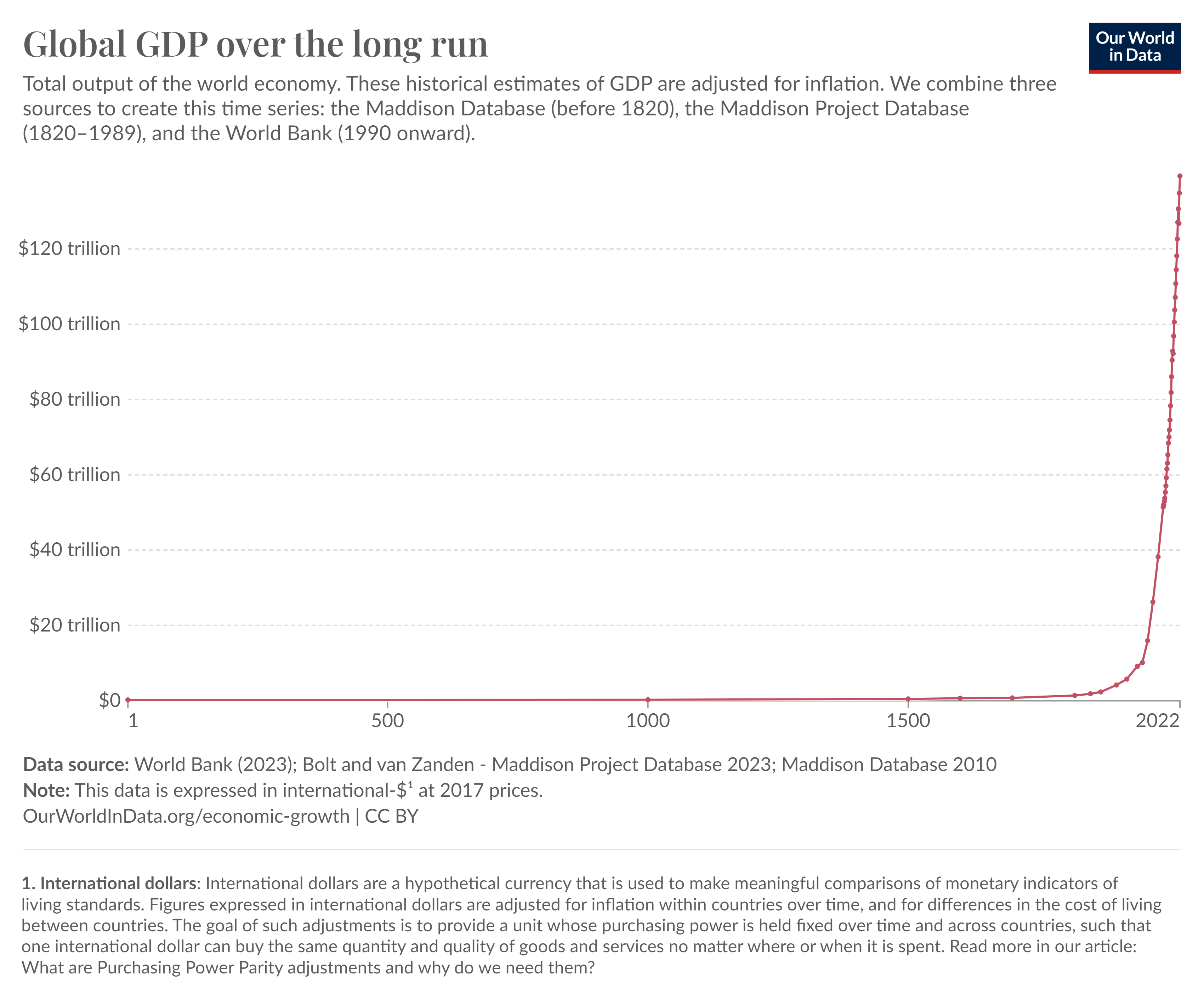

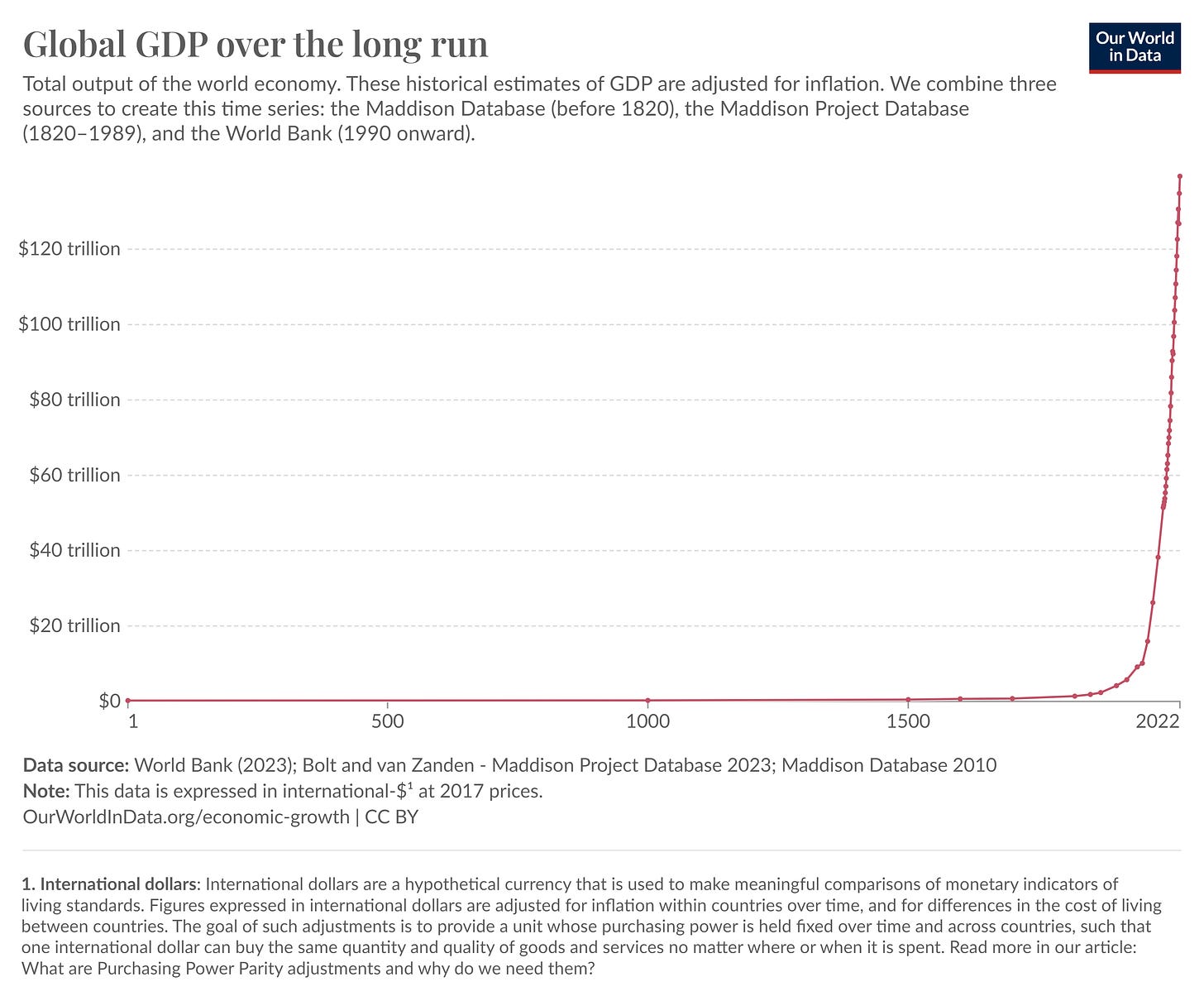

The World’s Greatest Graph - by J. Michael Wahlen (substack.com)

In the age of data science, visualizations have become crucial in interpreting and communicating complex information. While some charts succeed in simplifying data, others fail by being misleading or dull. The best visualizations tell a compelling story, much like the graph of world GDP over time, which Wahlen hails as the greatest.

Why the Graph is Exceptional

Simplicity and Elegance:

The graph uses a single dataset, a linear scale, and a monochrome color scheme, yet it narrates the entire journey of world economic growth.

Key Quote: "As elegant as Chanel’s little black dress, it has only one dataset... But, through the use of a single line, it tells us the entire journey of the world."

Historical Perspective:

For most of history, world GDP was almost stagnant, reflecting the harsh realities of life in the past.

Key Quote: "The world GDP line is basically zero for the first 1,500 years. That’s not bad, that’s catastrophic."

Current Prosperity:

The graph illustrates unprecedented economic prosperity today, affirming that this is the best time to be alive in economic terms.

Key Quote: "The most recent data point is the highest one; we live in the most prosperous time the world has ever known."

Growth Trajectory:

The graph shows a positive growth trend, with economic growth accelerating over time, especially due to rapid development in countries like China and India.

Key Quote: "The derivative is positive, and so is the second derivative - economic growth is increasing at an increasing rate."

Limitations of the Graph

GDP Limitations:

GDP doesn't encompass all aspects of human well-being, such as climate, health, and social factors.

Key Quote: "GDP is great but it has its limits. It does not tell us about climate, health, meaning, community, freedom, security, etc."

Not the Best of All Worlds:

Despite economic growth, the world faces challenges and could make better choices.

Key Quote: "Yes, this is the best time to be alive, but that does not mean we could not have made better choices or be making better ones now."

Progress is Not Inevitable:

Historical setbacks remind us that continuous progress is not guaranteed.

Key Quote: "Past performance does not guarantee future performance."

Varied Experiences:

Economic growth varies widely across regions and individuals, and GDP doesn't capture personal experiences.

Key Quote: "While this graph tells us about the world, it does not necessarily tell us about our own story."

Conclusion

The graph serves as a clear narrative of economic history, inspiring viewers to delve deeper into the reasons behind the trends. It underscores the importance of effective storytelling in data visualization.

Why It Matters

Understanding this graph helps contextualize current global economic conditions and challenges. It highlights the need for balanced perspectives on growth and development, urging us to consider broader aspects beyond mere economic metrics.

Overall, Wahlen's analysis encourages a thoughtful examination of how we interpret data and the stories we derive from it, emphasizing the significance of clarity and insight in visual storytelling.

Why It’s Usually a Mistake to Own Individual Stocks — Oblivious Investor

This article on the Oblivious Investor blog by Mike Piper, a CPA and personal finance author, advocates for investing in diversified stock market index funds/ETFs rather than attempting to pick individual stocks. Piper argues that individual stocks carry significant "diversifiable risk," which is not rewarded with higher expected returns and can be easily eliminated through diversification. He further explains why successfully picking winning stocks is much harder than most people think, making a strong case for a simple, low-maintenance approach to investing.

Key Points and Explanations:

1. Diversifiable vs. Undiversifiable Risk:

Explanation: Piper introduces the concept of diversifiable risk, which is specific to individual companies and can be mitigated by owning a diversified portfolio of stocks. He contrasts this with undiversifiable risk, also known as systematic risk, which affects the entire stock market and cannot be eliminated through diversification.

Key Quote: "Diversifiable risk is the risk of a specific stock earning poor returns. Undiversifiable risk (also known as systematic risk) is the risk that the stock market as a whole earns poor returns."

Why it Matters: This distinction is crucial because it lays the foundation for understanding why diversification is so important. By diversifying, investors can effectively eliminate diversifiable risk, leaving them exposed only to the unavoidable systematic risk of the market.

2. Only Undiversifiable Risk is Rewarded:

Explanation: Piper explains that while higher risk generally leads to higher expected return, this principle applies only to undiversifiable risk. Diversifiable risk, being easily eliminated through diversification, does not command a higher expected return.

Key Quote: "It is only nondiversifiable risk that is rewarded with greater expected returns."

Why it Matters: This point highlights the inefficiency of taking on unnecessary risk. Investors who focus on individual stocks are exposing themselves to higher diversifiable risk without being compensated for it, leading to a less favorable risk-reward profile.

3. The Difficulty of Picking Winning Stocks:

Explanation: Piper outlines two key reasons why consistently picking winning stocks is much harder than it seems. First, stock prices already reflect the market's consensus expectations about future earnings, meaning that investors need to possess unique insights to outperform the market. Second, the majority of stocks do not deliver exceptional returns, making it statistically unlikely for even seasoned investors to consistently pick winners.

Key Quote: "There is, therefore, little to be gained from picking individual stocks unless you know something that the rest of the market doesn’t — something that isn’t already 'priced in.'"

Why it Matters: This point debunks the common misconception that picking stocks is a simple matter of identifying promising companies. It emphasizes the need for specialized knowledge, access to information, and a high degree of luck to consistently outperform the market through individual stock selection.

4. The Market is Smarter Than You Think:

Explanation: Piper emphasizes that "the market" is not composed solely of amateur investors. A significant portion of stock market activity is driven by professional investors with deep expertise, access to vast amounts of data, and sophisticated analytical tools. Outperforming these professionals consistently is a daunting task.

Key Quote: "And “the market” does not primarily consist of people like your coworker Jimmy of dubious financial savvy. The vast majority of dollars moving around in the market are being moved by very intelligent people, who do this as their full-time job, and who generally have better and faster access to relevant information than you do."

Why it Matters: This point underscores the futility of trying to outsmart the market through individual stock selection. The odds are stacked against individual investors, making a diversified approach a more prudent and realistic strategy.

5. Most Stocks Don't Deliver Exceptional Returns:

Explanation: Piper cites research showing that a small percentage of stocks account for the majority of market returns over long periods. This means that even if an investor picks a handful of individual stocks, they are likely to miss out on the few superstar companies that drive overall market growth.

Key Quote: "The best-performing 4% percent of stocks explain the entire equity risk premium since 1926, as other stocks collectively earned no more than Treasury bills."

Why it Matters: This point highlights the statistical disadvantage of individual stock picking. The vast majority of stocks deliver mediocre returns, making diversification a more reliable strategy for capturing the overall growth of the market.

6. The Benefits of Index Fund Investing:

Explanation: Piper advocates for investing in "total stock market" index funds/ETFs as a simple and effective way to eliminate diversifiable risk, capture the market's overall return, and avoid the challenges of individual stock selection.

Key Quote: "As far as I’m concerned, if I’m going to own stocks: I don’t want any diversifiable (uncompensated) risk in my portfolio, I want to be sure that I’ll own whichever stocks happen to be the future superstars, and I don’t want to put myself in a position where I have to outsmart the market. So I just use boring “total stock market” index funds/ETFs."

Why it Matters: This point offers a practical solution for investors seeking a low-maintenance, diversified approach to investing. Index funds provide broad market exposure, eliminate the need for stock picking, and offer a favorable risk-reward profile for long-term investors.

Conclusion:

Piper's article makes a compelling case for the benefits of diversification and index fund investing. By understanding the distinction between diversifiable and undiversifiable risk, investors can make more informed decisions and avoid taking on unnecessary risk. Index funds offer a simple, effective, and low-maintenance approach to capturing the market's overall return without the challenges and uncertainties associated with individual stock selection.

What is Stoic Investing? (And how Stoicism can make you wealthy) - Darius Foroux

This article by Darius Foroux, author of "The Stoic Path to Wealth," explores the concept of Stoic investing, applying the principles of Stoicism to build long-term wealth and financial freedom. Foroux argues that Stoicism, with its emphasis on controlling emotions, focusing on what's within our control, and accepting what we can't change, provides a powerful framework for making sound investment decisions and achieving financial stability.

Key Points and Explanations:

1. Stoicism and Wealth-Building:

Explanation: Foroux introduces the concept of Stoic investing, explaining how the principles of Stoicism can be applied to wealth-building. He emphasizes that Stoicism, with its focus on long-term thinking and emotional control, can help investors make rational decisions and avoid common pitfalls driven by fear and greed.

Key Quote: "Being a Stoic makes you better at money, wealth-building, and investing. Stoic Investing strategies teach us to manage our emotions and focus only on things within our control (and let go of those that we cannot)."

Why it Matters: This point establishes the connection between Stoicism and investing, highlighting how the philosophy's core tenets can be leveraged to achieve financial goals. It sets the stage for exploring specific Stoic investing strategies and principles.

2. Practical Applications of Stoic Investing:

Explanation: Foroux outlines several practical applications of Stoic investing, such as investing for long-term wealth rather than immediate gratification, speculating only with money one can afford to lose, staying invested during market downturns, and investing consistently over time.

Key Quote: "Invest to build long-term wealth, not to make major purchases — Many people invest with the goal to make a lot of money so they can buy a bigger house, a new car, or to travel more. As a Stoic investor, you shouldn’t look at investing like that. Simply see investing as a way to compound your money so you can buy freedom, not things."

Why it Matters: This point provides actionable advice for applying Stoic principles to real-world investment decisions. It emphasizes the importance of long-term thinking, risk management, and emotional discipline in building sustainable wealth.

3. The Stoic Perspective on Money:

Explanation: Foroux explores the views of ancient Stoic philosophers on money, highlighting their emphasis on living a simple, frugal life and not being overly attached to material possessions. He clarifies that Stoics were not averse to money but rather advocated for non-attachment, recognizing that financial stability is necessary for freedom and well-being.

Key Quote: "Wealth consists not in having great possessions, but in having few wants." - Epictetus

Why it Matters: This point provides historical context and philosophical grounding for the concept of Stoic investing. It clarifies that Stoicism is not about rejecting wealth but rather about cultivating a healthy relationship with money, recognizing its value without becoming enslaved by it.

4. The Stoic Triangle of Wealth:

Explanation: Foroux introduces the "Stoic Triangle of Wealth," a framework for building wealth while living a fulfilling life. The three components of this triangle are: focusing on true desires, compounding earnings, and protecting capital.

Key Quote: "This idea allows us to live a life that’s both fulfilling and financially abundant."

Why it Matters: This framework provides a holistic approach to wealth-building, emphasizing the importance of aligning financial goals with personal values, generating passive income through investments, and managing risk to safeguard assets.

5. Five Key Principles of Stoic Investing:

Explanation: Foroux outlines five key principles of Stoic investing: focusing on what you can control, managing your emotions, remaining consistent and fearless, viewing market volatility as an opportunity, and focusing on the real value of a business.

Key Quote: "Stoic investing is all about accepting that markets will always go up and down. Instead of worrying about drops in the market, Stoic investors see them as chances to buy assets cheaply."

Why it Matters: These principles provide specific guidance for applying Stoicism to investment decisions. They emphasize the importance of emotional control, long-term perspective, rational analysis, and a focus on intrinsic value over market hype.

6. Living Well vs. Mindless Consumerism:

Explanation: Foroux contrasts the Stoic ideal of living well with the pitfalls of mindless consumerism. He argues that true contentment comes from appreciating what one has rather than constantly seeking more, emphasizing the importance of investing in experiences and relationships over material possessions.

Key Quote: "The truth is, we don’t really own anything. We’re just passing through, and the things we buy and call “ours” aren’t truly ours."

Why it Matters: This point highlights the philosophical underpinnings of Stoic investing, emphasizing the importance of aligning financial goals with a life of meaning and purpose. It encourages readers to reflect on their values and prioritize investments that contribute to genuine well-being.

Conclusion:

Foroux's article provides a comprehensive overview of Stoic investing, offering practical advice and philosophical insights for building wealth and achieving financial freedom. By embracing the principles of Stoicism, investors can cultivate emotional discipline, make rational decisions, and focus on long-term goals, ultimately leading to a more fulfilling and financially secure life.

What's a Carry Trade? (thediff.co)

This article from Byrne Hobart's "Capital Gains" newsletter, published on The Diff, explains the concept of a carry trade, a strategy where investors borrow money in a low-yielding currency and invest it in a higher-yielding one, aiming to profit from the interest rate differential. While this strategy can be profitable, Hobart cautions that it carries significant risks, particularly during periods of global financial stress.

Key Points and Explanations:

1. The Mechanics of a Carry Trade:

Explanation: Hobart describes the basic mechanism of a carry trade: borrowing in a low-yielding currency (often referred to as the "funding currency") and investing in a higher-yielding one. The difference in interest rates represents the potential profit, but it also reflects the market's expectation of the higher-yielding currency's depreciation over time.

Key Quote: "The basic idea of a carry trade is to make a list of currencies, ranked by yield. Borrow one of the lower-yielding ones, use it to invest in the higher-yielding one, and… that’s the trade."

Why it Matters: This point introduces the core concept of the carry trade, highlighting the simplicity of the strategy and the potential for profit based on exploiting interest rate differentials.

2. The Carry Trade Paradox: Why It Works (Sometimes):

Explanation: Hobart acknowledges that while the interest rate differential should theoretically reflect the expected depreciation of the higher-yielding currency, historically, this hasn't always been the case. He explains that investors often prefer to hold stable, low-yielding currencies, creating a demand for these currencies that can offset their expected depreciation.

Key Quote: "It just turns out not to be true, historically speaking: over time, the 'funding currencies,' i.e. low-rate currencies issued by a handful of very stable countries, did outperform flightier ones, but typically by less than the magnitude of that interest rate differential."

Why it Matters: This point explains the seemingly paradoxical nature of the carry trade: why it can be profitable even though the higher-yielding currency is expected to depreciate. It highlights the role of investor preference for stability and the demand it creates for "funding currencies."

3. The Risks of Carry Trades: Correlation and Crisis:

Explanation: Hobart outlines the inherent risks associated with carry trades, particularly during periods of global financial stress. He explains that when investors flee to safe-haven assets like the US dollar, euro, or yen during crises, emerging market currencies tend to depreciate simultaneously, creating a negative correlation that can wipe out carry trade profits.

Key Quote: "But there will also be times when all of these currencies are depreciating at once: when there’s a global financial crisis and every investor is liquidating risky investments in order to pay debts, those investors are disproportionate sellers of emerging market assets, and disproportionate buyers of dollars, euros, and yen."

Why it Matters: This point highlights the vulnerability of carry trades to global economic shocks. It emphasizes the importance of understanding correlation and the potential for simultaneous depreciation of multiple currencies, leading to significant losses.

4. Carry Trade Returns as Insurance Premiums:

Explanation: Hobart argues that the excess returns sometimes generated by carry trades can be viewed as a form of insurance premium. Investors are essentially compensated for the risk of holding currencies that are more likely to collapse during periods of global financial instability.

Key Quote: "That helps explain why the excess returns from carry trades never quite dropped to zero: the excess return they earn is really a kind of insurance premium…"

Why it Matters: This point provides a different perspective on carry trade returns, framing them as a reward for taking on the risk of holding volatile currencies that are more likely to depreciate when other assets are also losing value.

5. The Moving Target of Funding Currencies:

Explanation: Hobart highlights the dynamic nature of funding currencies, using the example of the Japanese yen. He explains that factors that initially made the yen attractive as a funding currency, such as low interest rates and a stable economy, can change over time, making the analysis of the carry trade more complex and unpredictable.

Key Quote: "But this means that analyzing the funding currency means tracking a moving target: a few years ago, you were looking at Japan as a slow-growth, rapidly-aging country whose households invest a wild share of their assets in cash and cash equivalents... But, over time, what you were looking at changed…"

Why it Matters: This point underscores the importance of continuous monitoring and analysis when engaging in carry trades. The factors that make a currency attractive as a funding currency can shift over time, requiring investors to adapt their strategies and risk assessments accordingly.

6. The Unwinding of Carry Trades: Policy Shifts and Momentum Reversals:

Explanation: Hobart explains that carry trades can unwind abruptly when central banks shift monetary policy or when the momentum driving the depreciation of the funding currency reverses. He cites the recent example of the Bank of Japan's interest rate hike, which led to a sharp appreciation of the yen and losses for those who had bet on its continued depreciation.

Key Quote: "The most recent iteration of the yen trade unwound brutally over the last few days, after the Bank of Japan increased interest rates by 25 basis points."

Why it Matters: This point emphasizes the sensitivity of carry trades to policy changes and market sentiment. It highlights the potential for sudden and significant losses when the underlying assumptions driving the trade are invalidated.

Conclusion:

Hobart's article provides a clear and insightful explanation of carry trades, highlighting both their potential for profit and the inherent risks involved. He emphasizes the importance of understanding the underlying economic factors driving currency valuations, the potential for correlation and crisis-driven losses, and the dynamic nature of funding currencies. By recognizing these complexities, investors can make more informed decisions about whether and how to engage in carry trades, balancing the potential for profit with the need for careful risk management.

Wealth Is A Single Player Game - A Teachable Moment (tonyisola.com)

In this blog post on "A Teachable Moment," Anthony Isola, CFP and head of the Educator/403(b) Division at Ritholtz Wealth Management LLC, argues that true wealth encompasses more than just financial abundance. He emphasizes that lasting happiness and contentment are crucial components of real wealth and can only be achieved by prioritizing internal validation over external validation. Isola encourages readers to shift their focus from competitive "multi-player" games to the "single-player" game of self-improvement and personal fulfillment.

Key Points and Explanations:

1. The Fallacy of Multi-Player Games:

Explanation: Isola argues that many people chase external validation, seeking approval and recognition from others, which he frames as playing "multi-player" games. He contends that this pursuit is ultimately futile, as true happiness cannot be found in the opinions of others.

Key Quote: "The reason for much of our misery is we spend too much time playing multi-player competitive games."

Why it Matters: This point challenges the common societal notion that external factors like status, possessions, or recognition measure success and happiness. It highlights the importance of shifting focus inward and seeking validation from within rather than relying on the fleeting opinions of others.

2. Happiness as a Single-Player Game:

Explanation: Isola posits that happiness is the ultimate "single-player" game, where the only competition is with oneself. He emphasizes that true contentment comes from aligning actions with personal values and pursuing goals that bring genuine fulfillment, regardless of external recognition.

Key Quote: "Only you can define what truly makes you happy. Happiness is the ultimate single-player game. Since external validation is nonexistent, you compete against yourself."

Why it Matters: This point emphasizes the importance of self-awareness and defining personal values. It encourages readers to take ownership of their happiness and pursue goals that align with their authentic selves, rather than seeking validation from external sources.

3. Material Wealth vs. Spiritual Wealth:

Explanation: Isola acknowledges that acquiring material wealth is achievable through disciplined financial habits, but he cautions that it doesn't guarantee happiness. He argues that true wealth encompasses both material and spiritual well-being, emphasizing the importance of cultivating inner peace and contentment alongside financial security.

Key Quote: "Many people are so caught up in others’ opinions that they’ve forgotten how to play single-player games. They expend all their energy competing against others, leading to situations where people cannot find peace and contentment in their lives, no matter how enormous their portfolio is."

Why it Matters: This point highlights the limitations of material wealth and emphasizes the importance of holistic well-being. It encourages readers to consider the non-financial aspects of their lives and invest in activities and relationships that contribute to their overall happiness and fulfillment.

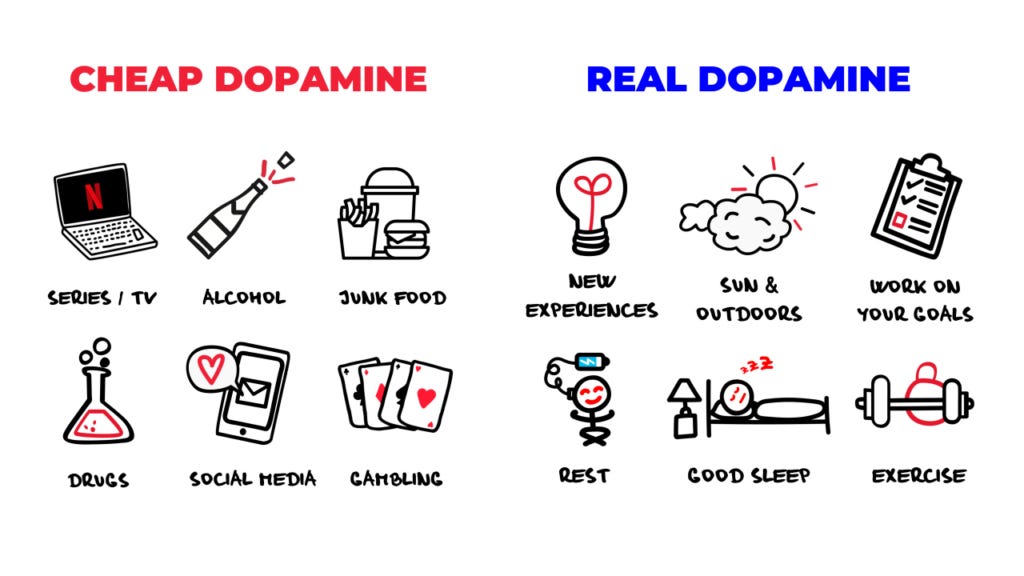

4. Happiness as a Learnable Skill:

Explanation: Isola argues that happiness is not a matter of luck or circumstance but a skill that can be learned and cultivated through conscious effort. He emphasizes the importance of building good habits, eliminating short-term dopamine hits, and engaging in activities that promote long-term well-being.

Key Quote: "Happiness is a learnable skill. Building good habits is integral."

Why it Matters: This point empowers readers to take control of their happiness and actively work towards creating a more fulfilling life. It suggests that happiness is not a passive state but an active pursuit that requires conscious effort and the development of healthy habits.

5. Replacing Bad Habits with Good Habits:

Explanation: Isola encourages readers to replace short-term dopamine-inducing activities like excessive social media use, video games, or unhealthy consumption with habits that promote long-term well-being, such as meditation, music, exercise, and spending time in nature.

Key Quote: "Essentially, you have to go through your life, replacing your thoughtless bad habits with good ones and committing to being a happier person." - Naval Ravikant

Why it Matters: This point provides practical advice for cultivating happiness by focusing on activities that promote mental and physical well-being. It emphasizes the importance of conscious habit formation and the power of replacing unhealthy behaviors with those that contribute to long-term fulfillment.

6. The Importance of Self-Care for Others:

Explanation: Isola argues that prioritizing personal happiness is not a selfish act but rather a necessary step towards creating a positive impact on the lives of others. He contends that when individuals are happy and content, they are better equipped to contribute to the well-being of their loved ones and their communities.

Key Quote: "Don’t consider this a selfish exercise. If you’re unhappy, the people you spend the most time with will suffer equally."

Why it Matters: This point reframes self-care as an act of service, highlighting the interconnectedness of individual well-being and the well-being of others. It encourages readers to prioritize their happiness not only for their benefit but also for the benefit of those around them.

Conclusion:

Isola's blog post challenges readers to redefine their understanding of wealth, emphasizing the importance of internal validation, personal fulfillment, and financial security. By shifting focus from competitive "multi-player" games to "single-player" games of self-improvement, individuals can cultivate lasting happiness and achieve true wealth materially and spiritually.